Squeeth Overview

What is Squeeth?

Squeeth is a new and exciting derivative product in the crypto space. It is known as a “power perpetual”, a type of derivative that is indexed to the power of an underlying’s price. In squeeth’s case the underlying asset is ETH, with squeeth aiming to track the price of ETH². Squeeth (standing for squared eth) is the first Power Perpetual, providing perpetual (never ending) exposure to ETH², with no strikes or expiries. Whether you want to go long or short squeeth, you will be exposed to ETH², referred to as the index price, functioning similarly to a perpetual swap. Squeeth is effectively making options perpetual. Thanks to the gigabrains at Paradigm (Dan Robinson, Dave White) & Opyn (Zubin Koticha, Andrew Leone, Alexis Gauba, Aparna Krishnan) for their development of squeeth, the first quadratic Power Perpetual in the history of DeFi and traditional finance).

Key Takeaways:

Squeeth (squared eth) is a “power perpetual” that aims to track the price of ETH².

No strikes, no expiries.

Squeeth is effectively making options perpetual.

Key Terms:

Squeeth stands for squared ETH.

oSQTH is a erc-20 token representing a squeeth position.

Index Price is ETH², the price squeeth aims to track.

Mark Price is the current trading price of squeeth.

Origins of Squeeth?

You could say the predecessors of squeeth are Everlasting Options and Power Perpetuals . Everlasting Options are a new type of derivative, introduced by SBF & Dave White from Paradigm. The product is the equivalent of perpetual futures for options. Everlasting options remove expiries, which is positive as liquidity can be less fragmented across multiple options. More liquidity means spreads will tighten and therefore provide a better product and user experience. However, fragmented liquidity cannot be completely avoided as different options contracts will still have different strikes.

Power Perpetuals were then introduced as the next logical step after Everlasting Options, released by Paradigm and Opyn. Power Perps remove the need for strikes in an options contract and are indexed to the power of an underlying’s price, such as ETH. If the price of ETH doubles, the power perp ETH² would 4x, if the price of ETH triples the power perp ETH^3 would 9x, and so on. The upside doesn’t come for free, as users who are long a power perpetual must pay funding to users who are short (that is if funding is positive, which in the case of power perpetuals, funding is almost always expected to be positive, aka longs pay shorts).

As you can see, squeeth effectively combines these concepts creating a quadratic power perpetual. Users long or short squeeth don’t need to worry about their position expiring at a certain date or at a specific price as strikes and expiries are non existent in the world of squeeth. This could have the effect of consolidating most of the options liquidity into a single erc-20, oSQTH.

Key Takeaways:

Squeeth’s predecessors are Everlasting Options and Power Perpetuals.

Everlasting Options are the equivalent of perpetual futures for options.

Fragmented liquidity is still a drawback in Everlasting Options as there are still multiple strikes.

Power Perpetuals remove strikes and are indexed to the power of an underlying price.

“There is no free lunch in finance” as longs have to pay shorts a funding rate for the potential upside.

Squeeth effectively combines these concepts creating the first quadratic Power Perpetual.

Squeeth has the potential benefit of consolidating much of the options liquidity into a single erc-20 token.

How Does Funding Work?

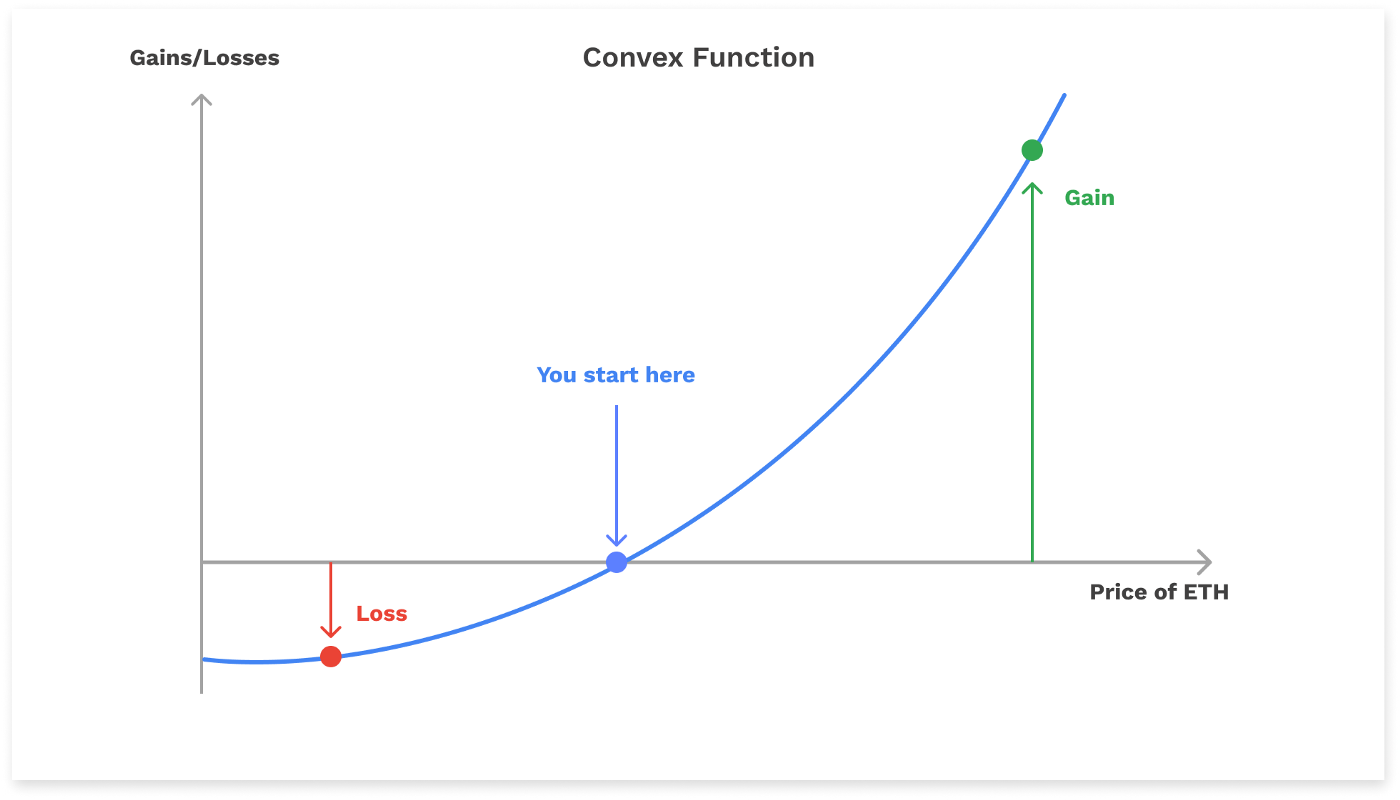

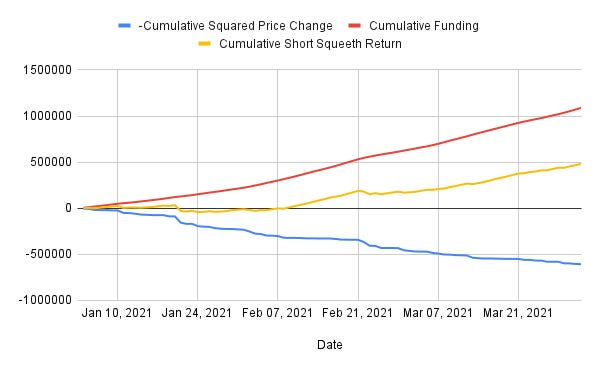

Funding Rate: Funding in squeeth is a payment made by users long oSQTH to the users who are short oSQTH. Supply and demand for the contract will create price movements in the contract and determine the difference between the Index Price (ETH²) and the Mark Price (squeeth). The difference between the Index Price and the Mark Price is what is known as the funding rate, and will be paid by users long squeeth to the users short. Because longs pay shorts to maintain their squeeth position, it is said that squeeth tracks ETH² and isn’t equal to it. Native to squeeth is a “convexity premium”, a term used to describe an asset with unlimited upside potential and protected downside (no liquidations). This is the reason longs are always expected to be paying shorts, as the potential unlimited upside unlocked does not and should not come for free. It is possible, though unlikely, that funding would flip negative and shorts would have to pay the longs to maintain their position.

In-Kind Funding: In-kind funding is something squeeth implements similar to a perpetual swap, but instead of being paid directly in cash, funding occurs through a continuous change in the contracts value. Changes in the price of the Index Price (ETH²) and the Mark Price (squeeth) give the same effect as a cash settled funding payment. Opyn has stated that they opted for in-kind funding because the overhead cost is much less (no extra machinery is required on the token to pay or receive funding). This also allows everything to fit into a standard erc-20 token contract.

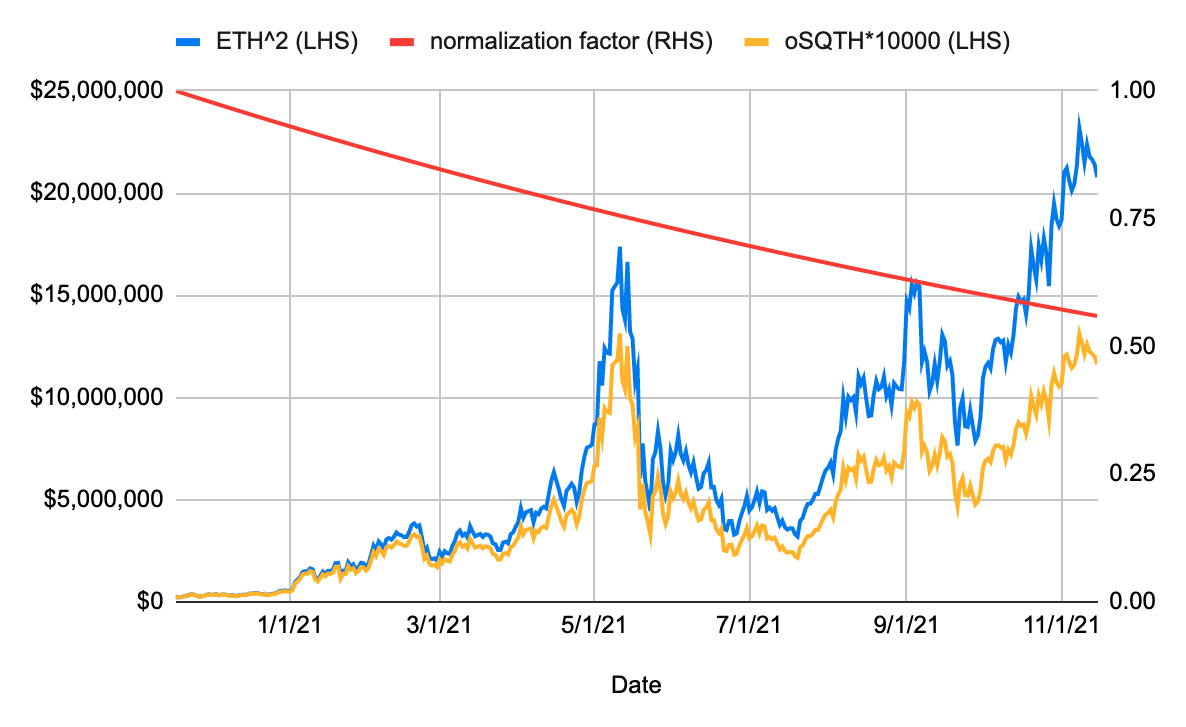

Normalization Factor: The normalization factor is how funding is implemented. It is a variable that adjusts the value of the debt of a squeeth position. A buyer of squeeth will have their oSQTH position gradually adjusted down relative to the index they aim to track (ETH²). For squeeth sellers the opposite will occur as the normalization factor will reduce the amount of debt owed on their short squeeth position as they receive funding from long positions.

Here the equation shows how the value of squeeth debt adjusts down with the normalization factor.

(value of debt in ETH) = (original debt amount) * (normalization factor) * (ETH price)

If a trader borrows 1 unit of squeeth the normalization factor changes from 1 to .99. After a weeks time this is equal to 1% funding. If the factor were to change from .99 to .96 the next week, that would be equal to another 3% of funding, and so on. In the above example, the funding rate during the first week is 1% (1 → .99), and 3% during the second week (.99 → .96). The difference between the normalization factor at two different points in time is the funding rate.

Key Takeaways:

Squeeth stands for squared ETH.

oSQTH is an erc-20 token representing a squeeth position.

Index Price = ETH², the price squeeth aims to track.

Mark Price = the current trading price of squeeth.

Native to squeeth is a convexity premium.

Funding is expected to be positive (long positions pay short positions).

Funding is paid in-kind via the value of the debt of a squeeth position gradually adjusting down over time.

The normalization factor is how funding is implemented.

The difference between the normalization factor at two different points in time is the funding rate.

What Can I Do With Squeeth?

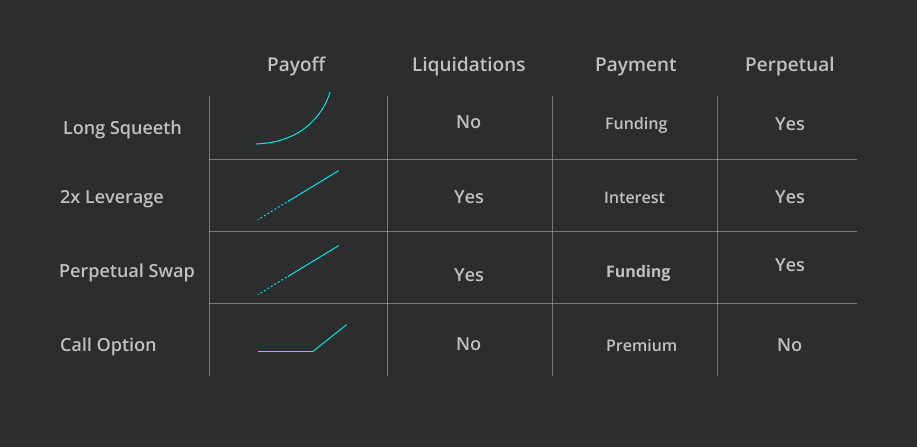

Going Long: Long squeeth is a leveraged ETH² position offering unlimited upside and protected downside with no liquidations. Essentially, long squeeth is a pure convexity trade (unlimited upside & capped downside). For the privilege of going long holders of oSQTH will pay an in-kind funding rate to the users who are short oSQTH. Funding is paid continuously (every time the contract is touched) and is expected to be positive (longs pay shorts) because of the potential upside. Comparing squeeth to a 2x leveraged position, we see that squeeth can offer more upside and less downside, though remember that you are paying a % of your position each day to keep this exposure, unlike a 2x leveraged position. Users want to be long squeeth when they expect high volatility in the price of the underlying asset (ETH). If price is expected to drop or go sideways, going long squeeth would not be attractive as you are exposed to the downside of the underlying while also paying a funding rate.

Going Short: Users can take a short squeeth (ETH²) position with ETH as their posted collateral. Unlike going long squeeth, users who are short have the chance of being liquidated. Users with short ETH² exposure earn a funding rate for holding the position, paid by the users who are long, with payments being in-kind and continuous. Users looking to short squeeth should look for environments in the market where volatility is low, preferably when the underlying asset is trading sideways or down. Even if the price of the underlying (ETH) rises while you are short oSQTH, you can still be profitable if volatility is low enough.

Key Takeaways:

Long squeeth is a leveraged ETH² position.

Compared to a 2x leveraged position, squeeth offers better upside and more downside protection.

Users long squeeth cannot be liquidated.

Users short squeeth can be liquidated.

Users want to be long squeeth when they expect high volatility to the upside in the underlying asset.

Users want to be short squeeth when they expect low volatility, preferably when the underlying asset is trading sideways or down.

Automated Strategies

Automated squeeth strategies are a way for users to earn yield in any market condition. Users can simply deposit ETH into the contract, which is automatically managed. Users who are long squeeth pay a funding rate to users who are short, with some of that funding being paid out to automated strategies, like the crab strategy. Lets talk about the crab strategy, the first automated squeeth strategy introduced by the team at Opyn.

Crab Strategy: The crab strategy is a market neutral strategy released by the team at Opyn in late January 20222, shortly after squeeth was released. Essentially a short vol strategy, the crab pairs a short squeeth position with a long ETH position, re-balancing often to maintain a delta of 0 to ETH and stay above a 1.5x collateral ratio. Expected to earn strong returns in a sideways market, the crab strategy aims to earn funding paid by users long squeeth, while remaining delta neutral to the underlying asset (ETH). In other words, you collect funding without being short ETH. Remember that funding is earned by being short squeeth, which is then paired with an ETH long, cancelling out any squeeth price exposure.

A sideways market, also known as a crab market, is the ideal market condition for the crab strategy to operate in (hence the name, crab). You are taking the view that volatility will be low, with the maximum payout being a constant ETH price. If the ETH price deviates more than the implied volatility in a single day, the strategy will lose money. As a user of crab you do not want to see volatile price moves in either direction, with a sideways market being the most ideal.

Future Strategies: Opyn has plans to release more strategies in the future, with two of them already being discussed, the bull strategy and the bear strategy. These have been topics of discussion in the squeeth community and in the Opyn discord, with release dates undecided. I expect these strategies to be very popular when released.

Advanced Strategies:

Squeeth is also able to provide other opportunities for more advanced users, such as:

LP on UniV3.

Hedge your UniV3 LP position.

Hedging any/all ETH/USD options with squeeth.

Using squeeth as a volatility oracle.

I am going to refer to Wade from the Opyn team for explanations of these strategies. Much more of an expert than I am, his squeeth primer is a must read, especially if you want to dive deeper into these advanced strategies. He did a fantastic job on it and has other great educational pieces on squeeth.

https://medium.com/opyn/squeeth-primer-a-guide-to-understanding-opyns-implementation-of-squeeth-a0f5e8b95684

CHARTS/DIAGRAM’S

Visualization of squeeth’s payoff structure...

Convexity Visualized (Squeeth Payoff Vs 2x Leverage)

Long Squeeth Payoff Visualized

Short Squeeth Payoff Visualized

Crab Strategy Payoff Visualized

Hedging Uniswap LP’s With Squeeth

Hedging All ETH/USD Options With Squeeth

Learning Resources:

https://medium.com/opyn/automated-squeeth-strategies-the-crab-strategy-is-now-live-b92281ebe701

Squeeth insides volume 1: funding and volatility | by Joseph Clark | Opyn | Medium,

JOIN THE OPYN DISCORD HERE: https://discord.com/invite/2NFdXaE

My Twitter: https://mobile.twitter.com/financekidd